Rethinking Medicare

Medicare was enacted a half-century ago and has been at the forefront of prominent political debates since the program first began paying hospital and physician bills for enrollees. Its rapid spending growth and its position as the dominant regulator of the nation's vast network of hospitals, clinics, and private physician practices have made it the focal point of both fiscal- and health-policy debates.

Proposals to reform Medicare have tended to focus on improving the program's operational efficiency and cost-effectiveness. The goal of these reforms has not been to change how Medicare works in any fundamental way but to make adjustments within the program's existing structure to facilitate the provision of higher-quality and lower-cost medical services.

That's an understandable strategy, but it is not the only way to think about reforming Medicare. It is also possible to take a step back and consider whether Medicare's basic structure ought to remain as it is indefinitely, and what an alternative design should entail. Both the fiscal prospects of the program and its effects on our broader health-care economy now call for such fundamental rethinking.

To do this, we would have to begin by considering just what the Medicare program actually consists of at the most basic level. At that level, Medicare is two things. First, it is a publicly run, community-rated insurance plan for persons age 65 and older and the disabled. Federal taxes and spending are not necessary to run this community-rated insurance plan. In theory, the full premium for this insurance could be collected from the enrollees during their time of eligibility for benefits. But Medicare isn't just a traditional health-insurance plan. It is also, secondly, a social-insurance program. Like Social Security, it is designed to provide additional support to households with more modest incomes and to subsidize, to a degree, the health care provided to all elderly and disabled Americans. These features of Medicare require the imposition of taxes to pay for program spending and open the program up to the demographic and other pressures that have made financing Medicare such a challenge.

An effective redesign of Medicare should begin by understanding that these two elements of the program are distinct. It could therefore be restructured to retain the protections associated with community-rated insurance while rethinking the tax-and-transfer elements associated with its current design. Disentangling these different facets would be complex programmatically, and would certainly be a very difficult political project. But it would also offer a way to modernize Medicare, make its finances sustainable, and enable it to help the larger health system work better for all Americans.

In the long run, such a reform would cut a Gordian knot that otherwise threatens to debilitate our politics in the coming decades.

THE MODEL OF SOCIAL SECURITY

Medicare's roots can be traced to the 1940s. During the immediate post-war period, many of the world's democratic governments were expanding social-welfare programs. In the United Kingdom, a newly elected Labor government pushed through the creation of the National Health Service, a single-payer program of universal, tax-financed health-care provision.

President Harry Truman sought to do something similar in the U.S. by proposing a series of measures in 1945 to improve access to health care. Among his proposals was a plan for a voluntary, federally administered National Health Insurance plan. Truman faced strong opposition to his plan in Congress. A major impediment was the American Medical Association, which opposed "socialized medicine." The general public was also skeptical about a large role for government in health care. Truman's plan went nowhere.

When Democrats were next in a position to push for broader health-insurance enrollment in the U.S., after the election of John Kennedy in 1960, they looked to a different kind of model — Social Security — rather than the fully nationalized health systems of Europe that inspired Truman.

Social Security was controversial when it was enacted in 1935, but President Franklin Roosevelt was always confident that its design — a pay-as-you-go social-insurance program — would eventually prove to be very popular and would, in time, make the program politically untouchable. He was right.

The key to Social Security's political success is, ironically, the payroll tax. Workers pay the tax during their working years, and then receive a benefit in retirement based, in part, on the wages that were taxed while they were working. This connection between taxed earnings and benefits paid in retirement is the core of Social Security. Most Americans believe they have "earned" their Social Security benefits when they reach retirement because the federal government withdrew taxes out of their paychecks to pay for it. Proposals from politicians to adjust Social Security payouts are thus viewed by voters with extreme skepticism.

The architects of Medicare borrowed liberally from the Social Security playbook. Medicare was built, in part, on an intergenerational social-insurance model. Current workers pay a payroll tax, which, in turn, determines their eligibility for some of the program's benefits (namely hospitalization coverage) when they retire. And the taxes they pay are deposited into a dedicated federal trust fund, from which the benefits for current retirees are paid. Much like Social Security, retirees believe they have earned their Medicare benefits with their payroll taxes, and thus also view attempts to alter those benefits as reneging on an implicit contractual agreement between citizens and the government.

While politically clever, using the Social Security template — namely, collecting payroll taxes from current workers to finance benefits for current retirees — to design Medicare has meant importing into Medicare the same demographic pressures now pushing Social Security toward insolvency.

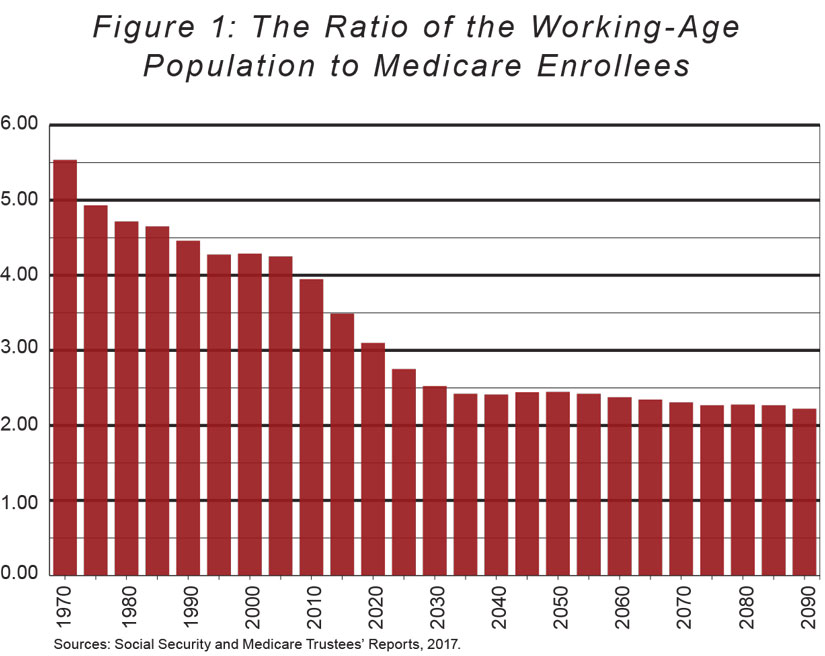

As shown in Figure 1 below, the combination of falling birth rates and rising life expectancy has dramatically reduced the ratio of the working-age population to Medicare beneficiaries. In 1970, there were 5.5 workers for every Medicare beneficiary. Today, there are just 3.5 workers for every person on Medicare, and by 2050, the ratio will have fallen to just 2.4.

Medicare has a second component — often called Medicare Part B — which pays for physician and other outpatient services, and which exacerbates the fiscal problems associated with hospital coverage. As originally conceived, Medicare Part B expenditures were to be financed partially from premiums paid by the beneficiaries themselves and partially from the federal Treasury. Working-age Americans were asked to directly subsidize the health-insurance premiums of elderly beneficiaries irrespective of those beneficiaries' ability to pay.

Initially, the idea was to have the program financed in equal amounts from the beneficiaries and from the federal Treasury. That policy held until 1976, when Congress, in response to rising costs (and thus also rising premiums for the beneficiaries), limited the annual increases in beneficiary premiums to the percentage increase in their Social Security benefits. This policy had the result of rapidly reducing the proportion of the program paid for by the enrollees themselves. In 1984, Congress established a new policy of keeping the beneficiary premiums at about 25% of Part B costs. That policy, with some exceptions, has basically held for the past three decades.

In 2003, Congress added a new drug benefit to Medicare, and modeled its financing on the Part B program. The prescription-drug benefit is referred to as Part D of the Medicare program. (Medicare beneficiaries also have the option to take their full entitlement in the form of enrollment in a private insurance option, called a Medicare Advantage plan. This feature of the program is often called Part C.) Part D beneficiary premiums are required for enrollment, but do not cover the full cost of the benefit. Once again, federal taxpayers pay whatever drug-benefit costs are incurred that are not covered by beneficiary premiums. The law was written to limit what program enrollees must pay to roughly 25% of the cost of the standard drug benefit, with federal taxpayers picking up the other 75%.

The burden on federal taxpayers from Medicare Parts B and D is enormous, largely hidden from view, and seldom noted in public debates. According to the 2017 Medicare Trustees' report, taxpayers will be providing an astonishing $4.4 trillion in subsidies for these parts of the program over the period from 2017 to 2026. These amounts exceed what will be spent during that same period on all of the federal programs providing direct support to low-income households combined.

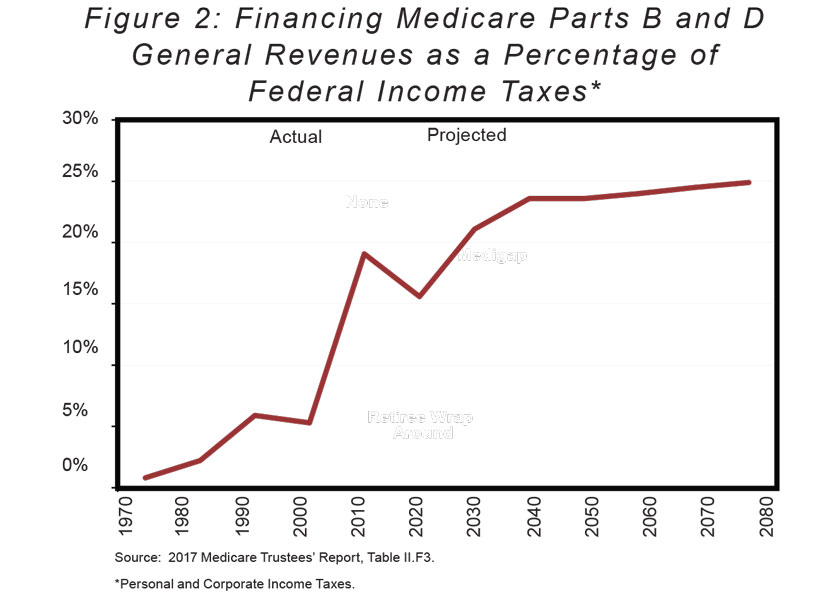

As shown in Figure 2 above, as recently as 2000, total general-fund payments to Part B amounted to just over 5% of federal income-tax collections (both personal and corporate). With the enactment of the drug benefit in 2003 and the retirement of the baby-boom generation, taxpayer subsidies for Medicare are set to soar. They are already well above 15% of all income-tax receipts and will approach 25% at mid-century.

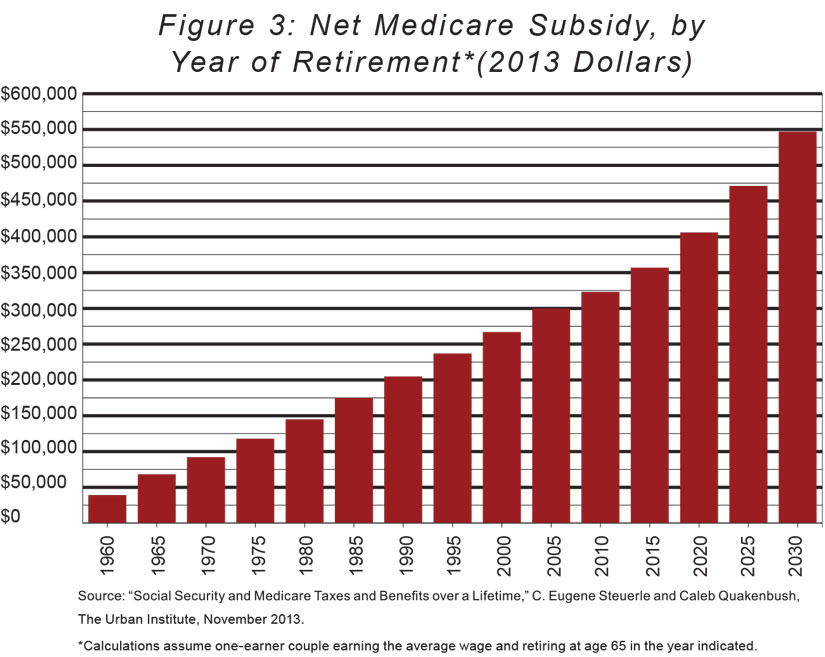

This subsidization covers a substantial portion of the average Medicare beneficiary's health insurance in retirement. As shown in Figure 3 below, a one-earner couple with average wages reaching age 65 in 2015 can expect to receive Medicare benefits that exceed what they pay in taxes by $357,000 (the figures shown are in constant 2013 dollars). And the net subsidy for such a couple will only go up in the years ahead.

In recent years, as Medicare's costs have mounted and recognition has spread that the program's financing rules are seriously unfair to working-age Americans, Congress has partially pulled back from the previous policy of providing substantial taxpayer assistance to all seniors regardless of their ability to pay for their own health care.

Both Parts B and D now charge higher-income seniors more for enrollment in the program. Under Part B, seniors with incomes above $85,000 (or $170,000 for couples) pay more than the normal premium of 25% of program costs that is charged to everyone else. The premium can go as high as 85% of program costs for seniors with the highest incomes. Part D utilizes the same income thresholds to increase premiums for these seniors to between 35% and 85% of costs. About 10% of all Medicare beneficiaries will pay these income-tested premiums in 2019, which means 90% of all Medicare beneficiaries will continue to receive the maximum amount of taxpayer subsidy for their health care. It is also noteworthy that even those seniors paying the highest possible Parts B and D premiums still receive a subsidy equal to 15% of the value of this insurance.

UNFUNDED LIABILITIES

Medicare was not built to be financed entirely by dedicated taxes and premiums from beneficiaries. There was always an expectation that some funding would come from the general fund of the Treasury. Still, it is useful to consider how much program expenditures will exceed the resources specifically dedicated to paying its costs in coming years.

The annual Medicare Trustees' reports estimate that the Medicare hospital-insurance (HI) trust fund has an unfunded liability of $3.6 trillion. That estimate assumes that a deep cut in hospital and other facility payments will occur without interruption for the next 75 years, which is unlikely. The actuaries therefore also make a calculation of the program's unfunded liabilities assuming this cut is eventually moderated. Under this alternative calculation, the unfunded liability of Part A of Medicare is about $4.7 trillion higher, or $8.3 trillion.

For Parts B and D of Medicare, the unfunded liabilities are essentially the cost of the program that is not covered by beneficiary premiums (and thus must be paid from the federal Treasury). The present value of all future general-fund payments to Medicare for Parts B and D of the program is $60.1 trillion.

This figure, combined with the HI trust fund's official unfunded liability of $3.6 trillion plus $4.7 trillion for removing unrealistic cuts in payment rates, means the total unfunded liability for the Medicare program exceeds $68 trillion.

A NEW APPROACH

Rethinking how Medicare might work in the future should begin with disentangling the program's two main features.

First, Medicare provides guaranteed inclusion in a nationwide, community-rated risk pool of all persons age 65 and older, plus eligible disabled workers. The program implicitly charges everyone in the risk pool the same premium for coverage, regardless of their health status. Moreover, no one can be denied access to the pool based on a prior history of illness. Inclusion in the Medicare risk pool is thus a highly valuable benefit, irrespective of the program's tax-and-subsidy system.

Second, Medicare is also a tax-and-transfer program. In a sense, the HI program can be thought of as a social-insurance program aimed at securing a type of annuity for health-insurance coverage in retirement. Workers pay the HI payroll tax while working and, in return, get an insurance benefit that has value equivalent to a monthly insurance premium, paid for by the government. While the implicit premium annuity is the same for all beneficiaries, higher-income workers pay much more in taxes to receive it. The combined employer-employee Medicare payroll-tax rate is 2.9% on covered wages for workers with incomes below $200,000 annually (the threshold is $250,000 for couples filing taxes jointly). Above these income thresholds, the tax rate rises to a combined 3.8%.

As noted, Medicare also collects premiums from beneficiaries and taps into the federal Treasury to pay for additional health-insurance benefits for this population. Medicare's tax-and-spending provisions are responsible for the program's near-constant state of financial distress.

Even if Medicare did not have its current tax-and-transfer features, it would still be a highly valued program for its beneficiaries. That's because beneficiaries would know that, at age 65, they would be guaranteed access to a health-insurance plan with predictable premiums based on overall costs for the entire enrolled population.

Conceptualizing Medicare in this way is useful because it immediately makes clear that a redesigned Medicare could de-emphasize its current tax-and-spending features, especially for those who could reasonably save enough to cover most of their health-insurance premiums in retirement on their own, while retaining and promoting its value as a source of guaranteed, affordable health insurance for the retired and disabled.

Reworking the program in this way would reduce the financial risks to federal taxpayers while still providing an important safety net to retirees.

The starting point for a fundamental and far-reaching reform of Medicare should be a vision for how the program would work after the reform is fully implemented (and following a lengthy transition period). Such a reform would involve six key features.

The first is a rationalized Medicare insurance product. Instead of separate insurance products for hospitalization, outpatient services, and drugs, Medicare would provide to enrollees a combined insurance product covering all of these essential medical services. A single premium would cover the cost of enrolling in Medicare insurance. Further, there would be a single, unified deductible; sensible cost-sharing; and catastrophic protection providing an upper limit on annual enrollee costs.

Second, Medicare would offer community-rated premiums for its beneficiaries. This simply means Medicare should treat everyone equally, regardless of their health status, just as is the case today. In practice, this means that insurance premiums for enrolling in Medicare would not vary based on the age or health status of enrollees. However, premiums should vary based on the lifetime earnings of enrollees, as well as on their own choices about the kind of coverage they prefer.

Third, a reformed Medicare program would involve a smaller universal entitlement funded entirely by a Medicare payroll tax. Even if there were no such basic entitlement, Medicare would remain an attractive program because of the security of the insurance it would offer. But to ensure maximum enrollment, the program should continue to provide a small, universal entitlement benefit to all enrollees, perhaps set to cover 20% or so of the value of today's benefit. According to the 2017 Medicare Trustees' report, the program spent about $12,900 per beneficiary in 2016. A benefit set at 20% of that amount would equal about $2,600 in today's terms. All Medicare enrollees in the future would be entitled to receive a premium subsidy of this amount (adjusted to reflect the value of the insurance plan at the time they are enrolled).

In 2017, Medicare spending equaled about $708 billion, while the Medicare payroll tax generated $301 billion in revenue. A Medicare program that cost 20% of today's program would equal $142 billion. It would therefore be possible to finance a universal entitlement at roughly 20% of today's benefit with a payroll tax set at roughly 60% of today's rate. However, because of the aging population, Medicare enrollment is projected to swell in coming years, as is Medicare spending. By 2040, there will be just under 60% more enrollees in the program. Therefore, a benefit set at 20% of the per-person value of Medicare under current law might require a payroll tax roughly equivalent to a combined employer-employee rate of 2.3%.

This new, smaller, universal entitlement should be paid from a single Medicare trust fund, and the long-term financing goal should be to cover program costs entirely from payroll-tax collections. In other words, when fully phased in, a redesign of Medicare should seek to eliminate entirely the general-fund subsidies that now dominate the program and impose an enormous financial burden on working-age Americans. Like Social Security, Medicare should provide a benefit that is self-sustaining over time with the payroll taxes dedicated to paying for it. There would be no need for two different trust funds under this kind of reform; Parts A and B could be merged together into a single Medicare trust fund.

If Medicare were restructured in this way, the program would still lead to substantial redistribution of resources among Medicare participants because higher-wage workers would pay substantially more in payroll taxes than lower-wage workers for a benefit that provides the same insurance value for all enrollees.

Retaining the payroll tax as the primary source of Medicare funding would also keep in place the strong political support that sustains the program today. Workers would continue to perceive that their payroll taxes were financing their benefits in retirement. In fact, under a restructured program, this prevailing perception would be more true than it is today, because there would be less general-fund subsidization of the premiums of workers who could afford to pay more of the total Medicare premium themselves out of their retirement savings.

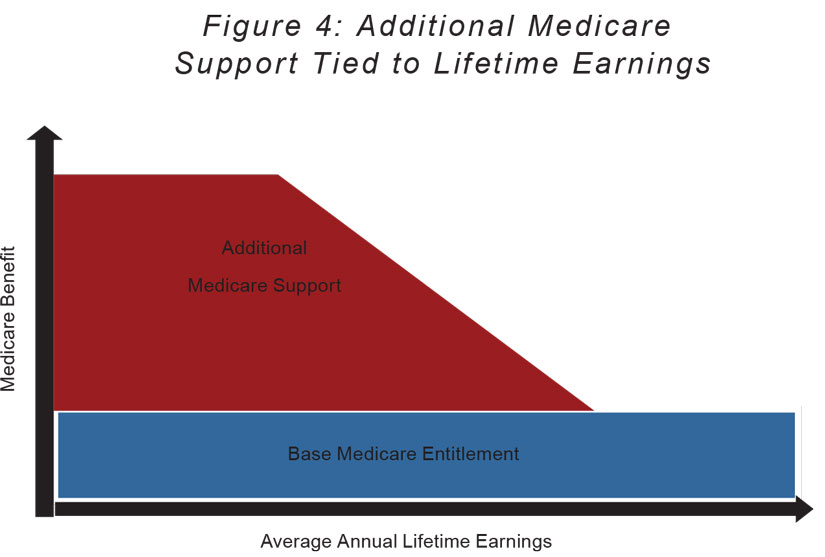

Fourth, a reformed program would offer additional financial support tied to lifetime earnings. Medicare should provide additional support to the elderly and disabled who lack the means to pay premiums on their own. This added benefit above the base level of entitlement would be calibrated to the lifetime earnings of the Medicare enrollee. Lifetime earnings is the appropriate measure because it avoids the disincentive effects and administrative complexity of measuring the actual savings and wealth of program enrollees. A means test of that nature would be intrusive and costly, and it would discourage enrollees from saving their earnings while working because of the resulting reduction in their Medicare benefits. Lifetime-earnings data are readily available from payroll-tax records and can be used to assess how much a person should have been able to set aside to pay premiums for health care in retirement, regardless of the actual state of their savings and wealth.

As depicted in Figure 4 below, the enrollees in roughly the lowest quartile of lifetime earnings would be eligible for substantial additional support on a sliding scale. That support would then be phased out so that middle-class and upper-middle-class seniors would get only the universal entitlement benefit.

The amount of support provided to enrollees with low lifetime earnings would be based on what it would cost to provide a low-cost-sharing, low-premium Medicare product. That could be ascertained by looking at the average actuarial cost of providing such a product through the traditional, government-managed fee-for-service program as well as the privately run Medicare Advantage plans.

Fifth, under these reforms, Medicare beneficiaries should receive their financial support (whether the base benefit or additional means-tested help) in the form of a defined-contribution payment. The beneficiary would be presented with a number of competing options for his Medicare coverage, and could use the defined contribution to reduce the cost of enrollment in the plan he finds most suitable and attractive. The level of support provided by the federal government would not vary based on the choice made by the beneficiary. Consequently, the beneficiary would be responsible for all of the additional premium costs associated with more-expensive options, and would keep all of the savings associated with enrollment in the less-expensive choices.

Both the base level of support and the added support for retirees with low lifetime earnings would be pegged to the price of an average-cost plan in the region. The traditional Medicare program, run by the federal government, would be one of the options available to beneficiaries. But there would be private plan offerings as well. The government's defined-contribution payment to the beneficiaries would be tied to a weighted average of the premiums charged for the various plans available (based on a standardized benefit). Those with the lowest lifetime earnings would get a defined-contribution payment close to the full premium cost of the average plan; that would be reduced gradually for beneficiaries with higher lifetime earnings until it reached about 20% of the total average premium for those with lifetime earnings that placed them in the middle class or higher.

While the government's defined-contribution payments would be pegged to a standard Medicare insurance plan, the private plans would be allowed to offer plans with varying levels of deductibles and cost-sharing. In particular, the private plan offerings could be in the form of high-deductible insurance (with a relatively low premium), combined with a Health Savings Account. Beneficiaries with defined-contribution payments in excess of the premium for the plan they select could deposit the excess in the HSA. And beneficiaries with HSA balances from their working years would be allowed to combine those accounts with a high-deductible Medicare offering.

The competition that would occur among the plans offered to the beneficiaries would help to hold down overall premiums. The Congressional Budget Office analyzed a reform plan built on defined-contribution payments and consumer choice — often called "premium support" — in 2017 and concluded that a reform plan that pegged the government contribution toward an average-cost plan would reduce overall costs by 8% compared to current law, and would reduce premium costs for beneficiaries by 7%.

Other reforms, such as modernization of the program's Medigap rules and improvements in the management of the government-run fee-for-service option, could supplement premium support and further reduce Medicare's long-term costs.

And finally, sixth, a Medicare program reformed along these lines would need to help Americans save more during their working years for health-care costs in retirement. This conceptual framework for Medicare is premised on the view that most (though not all) workers, with the right incentives, could and would save enough to finance their own health-insurance premiums in retirement if given the opportunity to do so. After all, most middle-class and upper-middle-class Americans pay for most of their private health-insurance premiums today out of their own resources while they are working.

In competitive labor markets, premiums paid by employers on behalf of workers come out of the total compensation the employers are willing to pay them. So it is the workers who are really paying for job-based health care, not the employers. Employer-paid premiums are not subject to federal income or payroll taxes, so there is an implicit subsidy of this coverage from the federal government, but it covers only about 40% of the cost of job-based health insurance. The average employer contributed about $5,500 toward health insurance per worker in 2017, which means workers paid for about $3,300 of that premium in lower wages, in addition to the $1,200 they had to pay directly in premiums themselves. Overall, then, the average worker is already paying about $4,500 toward health care annually, and that amount grows every year with the rise in health expenses.

It is not necessary to mandate that these households set aside more of their income for their Medicare premiums. Doing so would only encourage them to offset this required saving with adjustments in their other means of setting resources aside and building wealth. Rather, what is needed is transparent information about what their premium is likely to be for Medicare coverage in retirement, as well as the ability to set aside resources in tax-preferred savings vehicles that could be used to pay for that premium.

Many studies have documented that the existence of the Social Security program results in a reduction in retirement savings among workers. Scaling that program back, whatever one thinks of its other effects, would encourage higher savings among middle- and upper-middle-class workers. The same would be true with Medicare; a phased-in reduction in Medicare spending in the future would produce a rise in savings among workers who would expect to pay more for their health care in retirement. To make this easier, policymakers should adjust the allowable, tax-preferred savings vehicles to accommodate the need for additional savings for health premiums.

HSAs should be a primary means by which households set aside resources for premium expenses in retirement. Under current law, the maximum contribution allowable is $6,750 per year for a worker with family health-insurance coverage, and contributions can be made only if the worker is enrolled in a high-deductible insurance plan. Moreover, HSAs are poorly integrated with Medicare today. Withdrawals are permitted for Medicare premiums, but persons age 65 and older are not allowed to make continued contributions to their HSAs. These restrictions should be relaxed. Contributions should be permitted regardless of enrollment in a high-deductible plan and permitted for those age 65 and older. The contribution limit should also be raised substantially.

Tens of millions of workers also set aside substantial amounts in tax-preferred 401(k) and IRA savings vehicles. The contribution limits for these accounts could also be gradually increased for cohorts of workers expected to cover more of their Medicare premiums in retirement. In addition, withdrawals from these accounts for the payment of Medicare premiums could be exempt from federal taxation, thus putting these accounts on the same footing as HSAs and making them attractive vehicles for setting aside resources to finance higher premiums in retirement.

GETTING THERE

It is useful to conceptualize the reform of Medicare outlined above as most fundamentally a plan to substitute, in time, higher premiums from the middle and upper classes for the large general-fund subsidies taxpayers now provide to Medicare to finance the majority of Part B and Part D costs. The end goal is a self-financing Medicare program, paid for entirely from the receipts generated by the Medicare payroll tax (perhaps with a tax rate modestly below today's 2.9% rate). At that point, there would be no general-fund subsidies going to Medicare, burdening working-age Americans with added federal costs.

Viewed this way, it is possible to see how a transition from the current to the reformed program could proceed. Over time, as younger cohorts of workers began paying their Medicare payroll taxes, they would be advised of the expected premium they would owe when they became eligible for benefits in retirement. At the same time, older workers who are closer to retirement would be advised of a gradual reduction in the income thresholds used in the current program to establish higher premium requirements on enrollees with incomes above the thresholds. A gradual lowering of these thresholds would also mean a gradual lowering of the required general-fund subsidies necessary to keep the program afloat. After a number of years, the income thresholds used for the income-tested premiums would begin to approach the income parameters of the redesigned Medicare benefit. At that point, the program could move toward lifetime earnings as the basis for determining the required premium from beneficiaries.

As the years passed, there would be a gradual and steady increase in personal savings among younger workers in response to the expectation of a reduced Medicare benefit in retirement. At the same time, as retirees were subjected to gradually higher premiums based on their incomes, the general-fund subsidy for the program would decline, thus easing the implicit tax burden on working-age households. Although there is not a direct relationship between today's general-fund subsidies and the income-tax burdens placed on working Americans, a reduction in the subsidies would dramatically ease overall fiscal pressures, and certainly a tax reduction would be one possibility, thus perhaps offsetting to a degree the additional savings these households would need in order to pay for a higher proportion of their premiums in retirement.

Ultimately, there would come a time, perhaps in 30 years or so, when it would be possible to move fully to the redesigned Medicare program, as both workers and those entering Medicare coverage would have adjusted their expectations based on the new reality of the program's changed entitlement structure.

Other aspects of the redesigned program could proceed on a different, more-accelerated schedule. It should be possible to move quickly to a unified Medicare trust fund that combines all existing financing sources and program spending in one account. That would make the transition away from general-fund subsidization of the program more transparent, and set the stage for moving toward financing the program entirely from payroll-tax receipts.

It should also be possible to move toward a unified insurance product for new beneficiaries relatively quickly, and to implement a version of the premium-support model of beneficiary choice and plan competition, as a gradual transition from today's Medicare Advantage program. These changes would bring immediate program improvements and reduced costs that would pave the way for the rebalancing of the relative shares of the total cost burden borne by working-age taxpayers and the beneficiaries in terms of premium payments.

A DURABLE MEDICARE

It is not possible to turn back the clock to 1965 and start over on Medicare. The program is deeply embedded in the lives of the American people, making any kind of abrupt change highly unlikely and unwise. But there should be no doubt that Medicare, as currently constructed, creates immense fiscal problems for the United States that will need to be addressed one way or another.

In recent years, many policymakers have advanced Medicare reforms to make the program operate more efficiently. A prominent reform plan is the premium-support concept, which is described and advocated here as well. But if there was a window of opportunity during which enacting premium support might have addressed the core of Medicare's long-term fiscal challenge, that time is behind us. The basic problem with Medicare is structural, and goes beyond its overemphasis on government management of health insurance. Put simply, the program provides far too much subsidization to households that earned middle-class and upper-middle-class incomes while working. Today, all working-age taxpayers are subsidizing the insurance premiums of these households, which is the primary reason the program is such an immense fiscal burden.

However improbable it may first appear politically, it is possible to envision a different kind of Medicare structure, with less of its financing run through the federal budget but with still very tangible benefits that will be attractive for all seniors. That kind of program would be more sustainable, less burdensome on workers, and less distorting of U.S. health care. And because it would happen very gradually, the politics should not be unimaginable. Indeed, such changes are essential.